CQF项目课程学习介绍(二)—— 机器学习

| 阿里云国内75折 回扣 微信号:monov8 |

| 阿里云国际,腾讯云国际,低至75折。AWS 93折 免费开户实名账号 代冲值 优惠多多 微信号:monov8 飞机:@monov6 |

📧公众号进击的Matrix

🚫特别声明原创不易未经授权不得转载或抄袭如需转载可联系小编授权。

CQF与AI

上一篇文章CQF项目课程学习介绍(一)中粗略的介绍了CQF项目以及CQF Model 1- Model 3的课程学习内容。本篇文章将给大家介绍Model 4- Model 6的学习内容Model 4Model 5主要是机器学习也可称为人工智能的课程学习Model 6的内容固定收益和信贷。毫无疑问人工智能技术在量化金融分析中已大显身手CQF项目的课程内容也是紧跟行业前沿发展和趋势在正式课程和高级选修课程中都用了大量的课时模块来学习人工智能技术在量化金融分析中的应用。

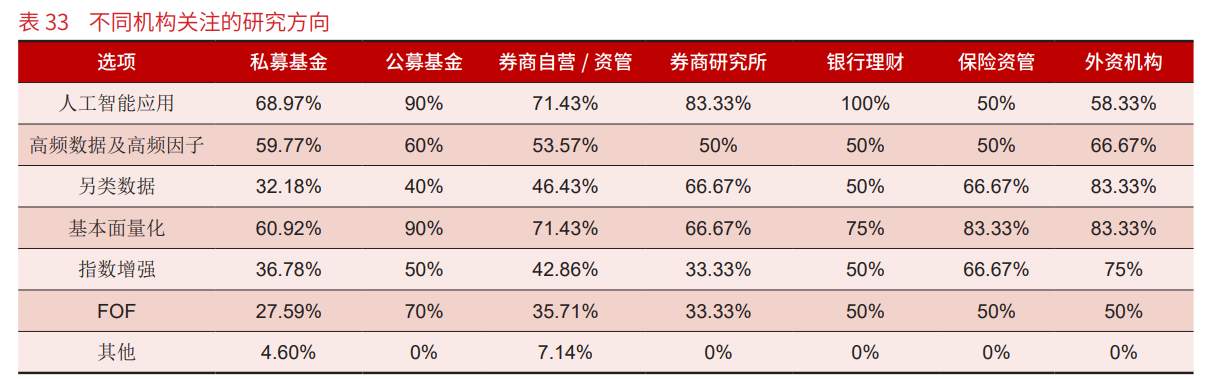

根据《2021年度中国量化投资白皮书》报告显示

国内相比于国外在布局人工智能技术上时间相对晚一些国外大型机构银行对冲基金布局相对较早并且技术体系比较完备同时国内对人工智能技术争议性相对较大主要体现在所有量化从业者在大面积主动学习人工智能但对于其趋势又感受并不强烈。可能源于在具体使用上一方面机构对于新型算法处于开拓期另外一方面又对其可解释性存疑所以使用较为慎重。

人工智能在量化金融研究中的应用主要在这两方面

- 模型构建

- 因子挖掘及生成

Module 4和Module 5的人工智能这两个模块对计算机技术以及编程的要求就比较高了对于有程序员背景或工科、理科背景的同学相对会更能接受些不会有太吃力的感觉如果没有接触过计算机技术、编程的同学CQF课程前导课的Python就显得尤为重要需要扎实学好可以多看几遍。

其实这也是CQF有人觉得难的原因因为要求学习者有较高的数学金融和计算机三大领域的专业性知识和较强的动手实践能力才能将该证拿下来。这也是它让我着迷之处我就是勇于不断挑战自己的知识边界认知边界不断扩张自己虽然不断扩张自己的过程是痛苦的但是当自己达到目标后是内心和精神上一场蜕变后的满足与强大我就是这么永无止境的不断前行前行前行的人

下面就来介绍CQF课程学习Module 4- Module 6的内容:

Module 4

Data Science and Machine Learning I

数据科学和机器学习 I

This module will introduce the latest techniques used for machine learning in finance. Starting with a comprehensive overview of the topic, the essential mathematical tools followed by a deep dive into the topic of supervised learning , including regression methods, K-Nearest neighbors, Support Vector Machines, Ensemble methods and many more.

本模块将介绍用于金融领域的机器学习最新技术。从对该主题的全面概述开始基本数学工具然后深入研究监督学习主题包括回归方法K近邻支持向量机集成方法等等。

- Introduction to Machine Learning: What is Mathematical Modeling, Classic Tools, Principal Techniques, Principal techniques for Machine Learning, Supervised & Unsupervised Learning, Reinforcement Learning.

机器学习介绍: 什么是数学建模经典工具主要技术机器学习的主要技术监督和无监督学习强化学习。

- Maths Toolbox: Maximum Likelihood Estimation, Cost/Loss Function, Gradient Descent, Stochastic Gradient Descent, Bias & Variance, Lagrange Multipliers, Principal Component Analysis.

数学工具箱: 最大似然估计损失函数梯度下降随机梯度下降偏差和方差拉格朗日乘数主成分分析。

- Supervised Learning I: Linear Regression, Penalized Regression: lasso, Ridge & Elastic Net, Logistic, Softmax Regression, Decision Trees, Ensemble Models -Bagging & Boosting.

监督学习 I: 线性回归惩罚性回归: 套索脊和弹性网逻辑回归softmax 逻辑回归决策树集成模型-装袋和升压。

- Logistic Regression, Support Vector Machines, Cluster Analysis: BIRCH, hierarchical, K-mean, Expectation maximization, DBSCAN, OPTICS and mean shift Kalman filtering.

逻辑回归支持向量机聚类分析: BIRCH 层次聚类算法分层K 均值期望最大化DBSCAN 基于密度的聚类算法OPTICS 和 Mean-Shift 和 Kalman 滤波器。

- Machine Learning Lab: Supervised Learning Implementation, Python - Scikit Learn; Support Vector Machines.

机器学习实验: 监督学习练习Python - Scikit Learn支持向量机。

Further Reading

- Trevor Hastie et al., The Elements of Statistical Learning: Data Mining, Inference, and Prediction, 2009 (2nd edition), Springer

- Martin Odersky et al., Programming in Scala: Updated for Scala 2.12, 2016 (3rd edition), Artima Press

- Macros Lopez de Prado, Advances in Financial Machine Learning, 2018, Wiley

- Christopher Bishop, Pattern Recognition and Machine Learning, 2006, Springer

- Max Kuhn and Kjell Johnson, Applied Predictive Analytics, 2013, Springer

Module 5

Data Science and Machine Learning II

数据科学和机器学习 II

In this module we will explore several more methods used for machine learning in finance. Starting with unsupervised learning, Deep learning and Neural networks, we will move into natural language processing and reinforcement learning. You will study the theoretical framework, analyze practical case studies exploring how these techniques are used within finance.

在本学习模块中我们将会探索机器学习用于金融中的更多方法从无监督学习、深度学习和神经网络开始我们将进入自然语言处理和强化学习。您将学习理论框架分析实际案例研究探索这些技术如何在金融中使用。

- Machine Learning & Predictive Analytics: Regression, regression in high dimensions, support vector machines, dimension reduction: principal component analysis (PCA), kernel PCA, non-negative matrix decomposition.

机器学习和预测分析归回高维回归支持向量机降维主成分分析(PCA)核主成分分析(Kernel PCA)非负矩阵分解。

- Unsupervised Learning I: K Means Clustering; Self Organizing Maps; Strengths & Weakness of HAC and SOM.

无监督学习 IK 聚类自组织映射HAC 和 SOM(自组织映射)的优势和劣势。

- Unsupervised Learning II: t-SNE; UMAP; Autoencoders.

无监督学习 II: t-SNE 降维学习方法UMAP 降维算法Autoencoders 自动编码器神经网络模型。

- Deep Learning & Neural Networks: Structural Building Blocks; Forward & Back Propagation; Multi Output Perceptron; Building Neural Networks.

深度学习和神经网络结构框架正向和反向传播多输出感知机构建神经网络。

- Neural Network Architectures: Feedforward, Recurrent, Long Short Term Memory, Convolutional, Generative Adversarial.

神经网络架构正反馈循环神经网络长短期记忆卷积神经对抗生成网络。

- Natural Language Processing: Pre-processing; Word Vectorizations, Word2Vec; Deep Learning & NLP Tools.

自然语言处理预处理词矢量化Word2Vec 算法模型深度学习和 NLP 工具。

- Reinforcement Learning: Multi-armed Bandit; Exploration Strategies; Risk Sensitivity.

强化学习: 多臂老虎机(MAB)探测策略风险敏感度。

- AI Based Algo Trading Strategies Using Python: Financial data analysis with Python and pandas, application of classification algorithms, vectorized backtesting, risk analysis for algo trading strategies.

使用 Python 的基于 AI 算法的交易策略使用 Python 和 pandas 进行金融数据分析分类算法的应用矢量化回归测试算法交易策略的风险分析。

Further Reading

- William McKinney, Python for Data Analysis, 2013 O’Reilly

- Foster Provost and Tom Fawcett, Data Science for Business, 2013, O’Reilly

- Gareth James et al., An Introduction to Statistical Learning, 2013, Springer

- Yves Hilipisch, Python for Finance, 2014, (2nd edition), O’Reilly

Module 6

Fixed Income and Credit

固定收益和信贷

In this module we will review the multitude of interest models used within the industry, focusing on the implementation and limitations of each model. You will learn about credit and how credit risk models are used in quant finance, including structural, reduced form as well as copula models.

在本模块中我们将回顾行业内使用的一些有趣模型重点关注每种模型的实现和有限性您将了解信用以及如何在量化金融中使用信用风险模型包括结构简化形式以及 copula 模型

- Fixed-Income Products: Fixed and floating rates, bonds, swaps, caps and floors, FRAs and other delta products.

固定收益产品固定收益率和浮动利率债券掉期合约利率上下限FRAs 和其他 Delta 产品。

- Yield, Duration and Convexity: Definitions, use and limitations, bootstrapping to build up the yield curve from bonds and swaps.

利率久期凸性定义使用和限制从债券和掉期合约中建立收益曲线。

- Curve Stripping: reference rates & basis spreads, OIS discounting and dual-curve stripping, cross-currency basis curve, cost of funds and the credit crisis.

曲线剥离参考利率和基础利差OIS 贴现和双曲线剥离货币基础曲线资金成本和信贷危机。

- Interpolation Methods: piece wise constant forwards, piece wise linear, cubic splines, smart quadratics, quartics, monontone convex splines.

插值法: 分段恒定向前分段线性三次样条曲线智能二次型四次曲线单调凸样条。

- Current Market Practices: Money vs. scrip, holiday calendars, business day rules, and schedule generation, day count fractions.

货币市场实践货币和代币假期日历工作日规则和日交易计划天计算分数。

- Stochastic Interest Rate Models, one and two factors: Transferring ideas from the equity world, differences from the equity world, popular models, data analysis.

随机利率模型一个和两个因素: 从股票世界转移观点不同于股票世界流行的模型数据分析。

- Calibration: Fitting the yield curve in simple models, use and abuse.

校准用简单模型拟合收益率曲线使用和滥用。

- Heath, Jarrow and Morton Model: Modeling the yield curve. Determining risk factors of yield curve evolution and optimal volatility structure by PCA. Pricing interest rate derivatives by Monte Carlo.

赫斯-伽罗-莫顿模型: 对收益率曲线的建模PCA 确定收益率曲线演变的风险因素和最佳波动率结构蒙特卡洛衍生品定价。

- The Libor Market Model: (Also Brace, Gatarek and Musiela). Calibrating the reference volatility structure by fitting to caplet or swaption data.

伦敦银行同业拆借利率市场模型: 还有布雷斯加塔雷克和穆西埃拉)通过拟合 caplet 或互换数据来校准参考波动率结构。

- Advanced Monte Carlo Techniques: Low-discrepancy series for numerical quadrature. Use for option pricing, speculation and scenario analysis.

高级蒙特卡罗技术: 数值求积的低差异级数用于期权定价投机和情景分析。

- SABR Arbitrage Free SABR Model: Managing volatility risks, smiles, local volatility models, reduction to the effective forward equation, arbitrage free boundary conditions.

SABR 无套利 SABR 模型管理波动率风险微笑局部波动率模型简化为有效的远期方程无套利边界条件。

- Credit Risk and Credit Derivatives: Products and uses, credit derivatives, qualitative description of instruments, applications.

信用风险和信用衍生品: 产品和用途信用衍生品工具的定性描述应用。

- Structural and Intensity models used for credit risk.

用于信用风险的结构和强度模型。

- CDS Pricing, Market Approach: Implied default probability, recovery rate, default time modeling, building a spreadsheet on CDS pricing.

CDS 定价市场方法隐含违约概率回收率违约时间建模建立 CDS 定价的电子表格。

- Synthetic CDO Pricing: The default probability distribution, default correlation, tranche sensitivity, pricing spread.

综合 CDO 定价违约概率分布违约相关性部分敏感性定价价差。

- Implementation: CDO/copula modeling using spreadsheets.

实践使用电子表格进行 CDO/copula 建模。

- Correlation and State Dependence: correlation, linear correlation, analyzing correlation, sensitivity and state dependence.

相关性和状态依赖相关性线性相关分析相关性敏感性和状态依赖性。

- Risk of Default: The hazard rate, implied hazard rate, stochastic hazard rate and credit rating, capital structure arbitrage.

违约风险风险率、隐含危险率、随机危险率和信用评级、资本结构套利。

- Copulas: Pricing basket credit instruments by simulation.

连接函数通过模拟定价一揽子信贷工具。

- Statistical Methods in Estimating Default Probability: ratings migration and transition matrices and Markov processes.

评估违约概率的统计方法: 分级迁移转移矩阵和马尔可夫过程。

- X-Valuation Adjustment: Background, default probability and exposure, collateral, CVA, regulatory requirements, DVA and FVA, Counterparty Lab in excel, credit default swaps, bootstrapping CDS spreads, interest rate swaps.

X-Valuation 调整背景违约概率和风险敞口抵押品CVA监管要求DVA 和 FVA对手 Lab in excel信用违约互换自举 CDS 价差利率互换。

Preparatory Reading

- Jon Gregory, The xVA Challenge: Counterparty Credit Risk, Funding, Collateral and Capital, third edition, 2015, Wiley (Chapters 4-7, 10, 12)

- Paul Wilmott, Paul Wilmott Introduces Quantitative Finance, 2007, Wiley (Chapters 14-19)

- Paul Wilmott, Paul Wilmott on Quantitative Finance, second edition, 2006, Wiley (Chapters 30-33, 36, 37, 39-42)

- Peter Jaeckel, Monte Carlo Methods in Finance, 2002, Wiley (Chapters 1-14)

Further Reading

- Avinash K. Dixit and Robert S. Pindyck, Investment Under Uncertainty, 1994, Princeton University Press

- Darrell Duffie & Kenneth J. Singleton, Credit Risk: Pricing, Measurement, and Management, 2003, Princeton University Press

- Gunter Loffler and Peter Posche, Credit Risk Modeling using Excel and VBA, 2007, Wiley

- George Chacko et al., Credit Derivatives: A Primer on Credit Risk, Modeling, and Instruments, 2006, Wharton School Publishing (Chapters 3, 5)

- Philipp J. Schoenbucher, Credit Derivatives Pricing Models: Model, Pricing and Implementation, 2003, Wiley (Chapters 2, 4, 5)

- Antulio N. Bomfim, Understanding Credit Derivatives and Related Instruments, 2004, Academic Press (Chapters 15, 16, 17)

- Nassim Taleb, Dynamic Hedging, 1996, Wiley

- John C. Hull, Options, Futures and Other Derivatives, fifth edition, 2002, Prentice-Hall

最后欢迎大家点赞、收藏、评论转发

欢迎大家关注我的微信公众号微信搜索进击的Matrix

欢迎大家关注我的知乎可乐